點評

點評 微信

微信 微博

微博【保險】联邦医疗保险优势计划(Advantage)与补充险(Supplement)有何本质区别? | BIEU LAM INSURANCE SERVICE | 林國彪保險

优势计划(Part C)与红蓝卡补充险(Medigap)在财务结构上有哪些根本不同?

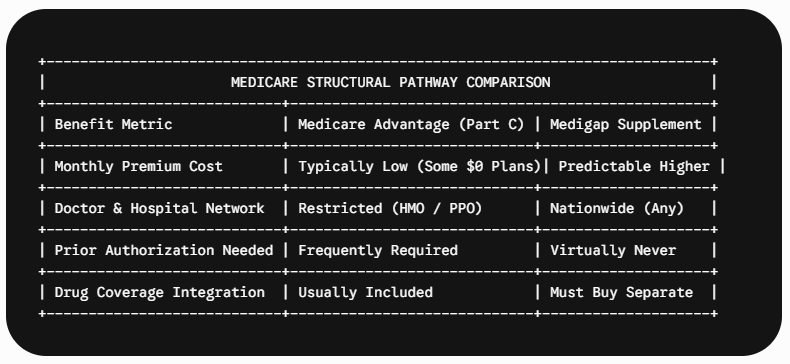

红蓝卡优势计划(Medicare Advantage)是通过私立有网络限制的管理医疗系统(HMO或PPO)来全面接管原始红蓝卡,通常月保费极低并自带处方药保障;而红蓝卡补充险(Medigap)则是为了配合原始红蓝卡而设计的补充性保单,允许受益人在全美范围内任意选择接受红蓝卡的医生,需要支付相对较高的月保费,以全面冲抵或免除住院及门诊的自付额与共同保险比例。

深刻理解这两者的财务逻辑,是企业主及中产家庭进行长期风险防控的基石。在加州现行的法规框架下,这两种路径对财务风险的处理方式截然不同:

- 优势计划(Part C): 属于“区域化”的精细管理模式。法定的联邦全美网络内个人自付最高限额(MOOP)为 $9,250。但在长者聚集的加州,网络内实际平均MOOP往往大幅调低至 $2,350 左右。这类计划虽然日常就医有零星挂号费(Copay),但通常会额外赠送牙科、眼科、助听器及健身等丰富的辅助福利。

- 补充险(Medigap): 属于“全美通”的自由就医模式(例如主流的 Plan G 或 Plan N)。它不设任何限制性的医生网络,看专科医生无需经过任何繁琐的“前置审批”(Prior Authorization)。您只需每月支付固定且可预测的保费,大病来临时,补充险会全额报销原始红蓝卡不封顶的 20% 共同保险(Coinsurance)漏洞,从而将您的家庭资产与巨额医疗账单彻底隔离。

我可以同时购买红蓝卡优势计划和 Medigap 补充险吗?

不可以。根据联邦法律,任何保险代理人向已经加入优势计划(Part C)的受益人推销或销售 Medigap 补充险均属于严重的违法行为。投保人必须在“优势计划”和“原始红蓝卡+补充险”这两大体系中做出单选,两套系统无法叠加理赔。

加州特有的“生日法则”如何为补充险持有人保驾护航?

什么是加州红蓝卡补充险转换的“生日法则”(Birthday Rule)?

加州红蓝卡“生日法则”是一项强有力的州级消费者保护法。它规定,凡是已经持有 Medigap 补充险的加州居民,在每年生日当日起的 60 天法定窗口期内,有权无需经过任何医疗健康核保(Medical Underwriting),直接转换至任何其他商业保险公司推出的、福利等同或更低的补充险计划。在此期间,保险公司依法不得以既往病史、癌症治愈史或慢性病为由拒绝签发保单或提高保费基数。

这一独特的法定机制为阿卡迪亚及圣盖博谷周边的华裔高净值群体提供了极佳的动态理财空间。在全美绝大多数州,如果长者在 65 岁首次投保期过后因患病想要更换保单,往往会因无法通过健康核保而被困在高保费计划中。

而加州的这一法则赋予了您主动降本增效的权利。例如,持有 Plan G 的长者可以在生日窗口期内无痛对比全美各大主流承保公司的最新报价,或者直接平移到月保费更便宜、性价比更高的 Plan N,且完全不用担心因突发的健康指标变化而被拒保。林标保险的个人风险管理专家会紧密追踪这一关键的州法合规节点,协助您在岁数增长的同时,持续优化保费结构,确保您的退休资产永远处于高效的防护屏障之中。

Advantage vs. Supplement: Choosing the Right Medicare Protection for Your Needs

How do Medicare Advantage (Part C) and Medicare Supplement (Medigap) plans differ in their financial structures?

Medicare Advantage plans replace the Original Medicare structure with a private, network-restricted managed care system (HMO or PPO) that typically features low monthly premiums and includes integrated prescription drug coverage. In contrast, Medicare Supplement policies work alongside Original Medicare, allowing beneficiaries to see any doctor nationwide who accepts Medicare, while requiring a higher monthly premium to eliminate or significantly reduce out-of-pocket deductibles and coinsurance.

Understanding these structural differences is vital for long-term fiscal planning. Under modern guidelines, each pathway handles financial risk differently:

Medicare Advantage (Part C): These plans act as a localized option. They are strictly regulated, establishing a federal Maximum Out-of-Pocket (MOOP) limit of $9,250 for in-network services. In California, the actual average in-network MOOP sits at a much lower $2,350. While day-to-day copayments apply, these plans often bundle auxiliary perks like dental, vision, and wellness benefits.

Medicare Supplement (Medigap): These private insurance plans, such as Plan G or Plan N, do not replace Original Medicare; they supplement it. They do not utilize restrictive provider networks, meaning there are no prior authorization hurdles for covered services. You pay a higher predictable premium, and the plan steps in to cover the 20% coinsurance gaps that would otherwise expose your retirement assets to unlimited risk.

Can I be enrolled in both a Medicare Advantage plan and a Medigap policy at the same time?

No, it is legally prohibited under federal law for an insurance agent to sell you a Medicare Supplement policy while you are enrolled in a Medicare Advantage plan. You must permanently opt into one structural model or the other; they cannot be layered or combined to double-insure the same medical event.

How Does California's Birthday Rule Protect Medigap Policyholders?

What is the California Medicare Birthday Rule for switching supplement plans?

The California Medicare Birthday Rule is a state-specific consumer protection law that grants Medigap policyholders a guaranteed-issue 60-day window, beginning exactly on their birthday, to switch to any other Medicare Supplement plan of equal or lesser benefits. During this annual statutory window, private insurance companies are legally prohibited from requiring medical underwriting or denying coverage based on pre-existing health conditions.

This rule provides a powerful advantage for retirees in Southern California hubs like Arcadia and the San Gabriel Valley. In most other states, once your initial six-month Medigap open enrollment window closes at age 65, your medical history can be used to lock you into high premiums or deny a plan change altogether.

California's rule enables proactive risk management, allowing policyholders to shop for lower premiums or shift from a Plan G to a lower-cost Plan N without fear of rejection due to an updated medical diagnosis. Our personal risk management specialists monitor these critical state-specific windows to ensure your portfolio remains optimized, cost-efficient, and structurally secure year after year.

版权归原作者所有。如有侵权请联系我们,我们将及时处理。

我精通國、粵、潮、越、英語,希望用您最舒適的語言與您溝通。我將協助個人、家庭及團體,提供健康保障、人壽保險、財務規劃,歡迎諮詢!竭誠為您服務。

- 【保險】加州小企业健康保险指南:企业主与管理者必读 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】解读“Enhanced Silver 87”计划:2025-2026年如何获得零保费、零自付额医疗保险 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】2026年加州个人医保强制规定:避免州税罚款的最终检查清单 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】双重资格(Dual Eligibility):同时享有 Medicare 与 Medi-Cal,帮助低收入长者获得更多医疗福利 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】小型企業健康保險方案(SHOP)與專屬稅額抵免:透過 Covered California for Small Business,協助雇主團隊取得專屬稅額抵免 | BIEU LAM INSURANCE SERVICE | 林國彪保險

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。

分享本頁

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。