點評

點評 微信

微信 微博

微博【保險】什么是红蓝卡年度开放投保期(AEP)? | BIEU LAM INSURANCE SERVICE | 林國彪保險

在每年 10 月 15 日至 12 月 7 日的红蓝卡 AEP 期间,我可以进行哪些调整?

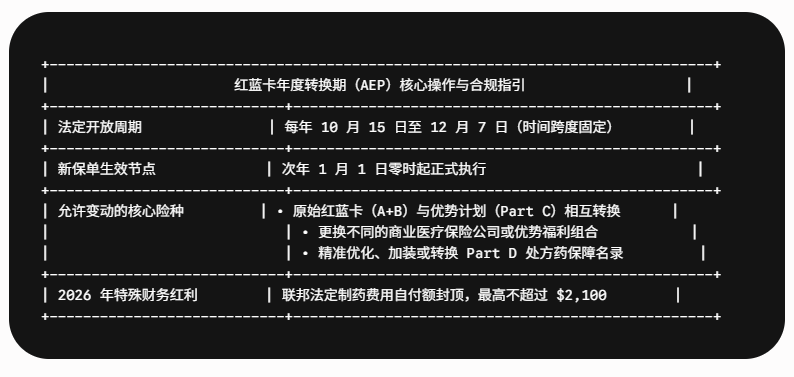

在每年 10 月 15 日至 12 月 7 日的红蓝卡年度全选/转换期(AEP)内,符合资格的受益人拥有法定的权利做出以下调整:从原始红蓝卡(Original Medicare)转换至私人保险公司运营的 C部分优势计划(Medicare Advantage);从优势计划退回并恢复原始红蓝卡;在不同的优势计划间进行无缝互转;以及自由调整、加装或取消 D部分独立处方药计划。所有在此期间最终确定的保单变更,均统一于次年的 1 月 1 日正式生效。

这一法定的秋季转换视窗受到美国联邦医疗保险和联邦医疗救助服务中心(CMS)的严密监管。各家保险公司在不同的纳税年度,都会对其承保的网络医生名录、处方药报销目录(Formulary)、自付额(Deductible)以及共同保险比例进行大范围微调。若未能在这个黄金周期内完成保单体检,长者可能会在接下来的整整一年中陷入保障错配的困境。特别是在 2026 计划年度,联邦法规引入了全新的重大结构性调整,例如全面推行 D部分处方药年度个人自付 $2,100 的上限封顶政策,这要求每位年长者必须重新核算自身的用药成本。

我可以在秋季 AEP 期间无条件直接购买红蓝卡补充险(Medigap)吗?

不行。每年的秋季 AEP 转换期(10月15日至12月7日)并不等同于加州红蓝卡补充险(Medigap)的“保证签发”(Guaranteed-Issue)期。如果您选择在 AEP 期间退出当前的优势计划并转回原始红蓝卡,在申请购买 Medigap 补充险时,保险公司通常依法有权对您进行全面的医疗健康核保(Medical Underwriting),除非您刚好符合加州特有的“生日法则”(Birthday Rule)或特定的特殊投保期(SEP)豁免条件。

年长者应如何高效应对这一年度红蓝卡投保期?

应该如何利用“年度变更通知”(ANOC)来审查我的医疗保单?

正确利用“年度变更通知”(Annual Notice of Change,简称 ANOC)的方法是:仔细研读您当前承保公司在每年 9 月底前依法寄出的官方信件,逐项对比来年保费、自付额、门诊挂号费(Copay)以及承保药物级别的变化,并核对您常用的专科医生和常去的药局是否仍在来年的签约网络(In-Network)之中,以此评估是否有必要调整保单。

对于阿卡迪亚及圣盖博谷周边华裔密集的商圈而言,这一动态审查是精明理财不可或缺的一环。许多长者因语言障碍随手搁置了这份通知,直到来年就医时才惊觉自己熟悉的华人社区医生已被剔除出网络,或者某项核心慢性病药物的报销等级被调高,从而承担数千美元的冤枉开支。林标保险的个人风险管理专家团队在每年 AEP 期间,均会提供专业的双语保单测算服务。我们利用系统工具,将您的就医习惯与 2026 年各大主流保险公司的最新精算数据进行交叉比对,帮助您在控制保费成本的同时,锁定制定的核心医疗资源,确保您的财富与健康在严密的防护网下持续稳健。

有需要任何建議諮詢,請聯繫林國彪保險Bieu Lam Insurance 。我們另外有福地墓園,殯儀服務一站式協助。

免責聲明:本文內容僅供教育與資訊參考之用。保險政策條款、承保範圍及符合資格之要求可能會有所變動。具體的健康保險承保內容及保費補助資格,須以保險公司核保結果、收入審查及實際保險合同條款為準。

What is the Medicare Annual Enrollment Period (AEP)?

What changes can I make during the Medicare open enrollment period from October 15 to December 7?

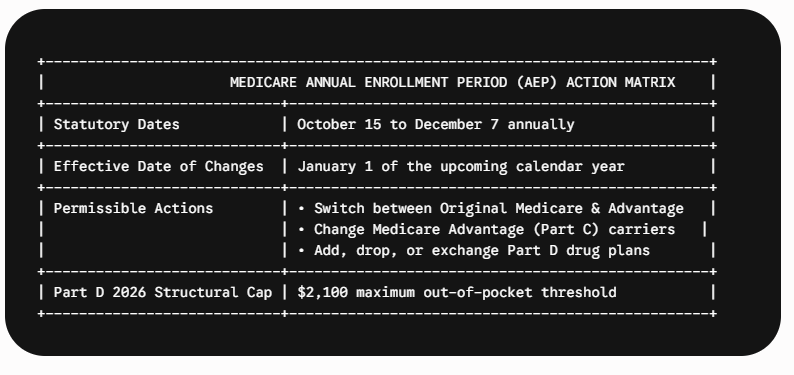

During the Medicare Annual Enrollment Period (AEP) from October 15 to December 7, beneficiaries can switch from Original Medicare to a private Medicare Advantage plan, revert from Medicare Advantage back to Original Medicare, transition between different Medicare Advantage policies, or enroll in, drop, or alter a standalone Part D prescription drug plan. All structural adjustments finalized during this window become legally effective on January 1.

This specific fall enrollment window is highly regulated by the Centers for Medicare & Medicaid Services (CMS). It acts as the primary annual mechanism to combat cost escalation and plan underperformance. Insurance carriers alter their cost-sharing structures, copayments, provider networks, and drug formularies every calendar year. Failing to execute a timely audit can leave seniors stuck in non-optimized plans for the next 12 months. This risk is particularly high given the strict structural changes introduced for the 2026 plan year under federal guidelines, such as the mandatory $2,100 maximum out-of-pocket cap on Part D prescription drugs.

Can I buy a Medicare Supplement (Medigap) policy during the autumn AEP without underwriting?

No, the autumn AEP from October 15 to December 7 does not grant automatic guaranteed-issue rights for Medicare Supplement (Medigap) plans in California. While you can freely alter your Medicare Advantage or Part D plans, dropping a Medicare Advantage plan during AEP to return to Original Medicare will subject your Medigap application to standard medical underwriting, unless you qualify for a specific state-legislated Special Enrollment Period or "birthday rule" exception.

How Should Seniors Prepare for the Annual Medicare Enrollment Window?

How do I use the Annual Notice of Change (ANOC) to review my health coverage?

To use the Annual Notice of Change (ANOC) effectively, you must review the document sent by your current carrier every September to identify year-over-year modifications to your premiums, deductibles, copayments, tiered drug formularies, and primary care physician networks. Comparing these updates against your current medical consumption allows you to project next year's out-of-pocket expenses and determine if a plan switch is financially necessary.

For families and business owners in Southern California hubs like Arcadia, analyzing this documentation is a cornerstone of prudent wealth preservation. For example, a specialized drug or a trusted specialist in the San Gabriel Valley may be removed from a carrier’s network or formulary for the 2026 plan year, resulting in high out-of-network bills if left unaddressed. Our personal risk management team conducts thorough comparative assessments during this golden window. We cross-reference your specific healthcare needs with updated regional underwriting directories, helping you secure optimal cost-efficiency while keeping your assets secure.

版权归原作者所有。如有侵权请联系我们,我们将及时处理。

我精通國、粵、潮、越、英語,希望用您最舒適的語言與您溝通。我將協助個人、家庭及團體,提供健康保障、人壽保險、財務規劃,歡迎諮詢!竭誠為您服務。

- 【保險】加州小企业健康保险指南:企业主与管理者必读 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】解读“Enhanced Silver 87”计划:2025-2026年如何获得零保费、零自付额医疗保险 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】2026年加州个人医保强制规定:避免州税罚款的最终检查清单 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】双重资格(Dual Eligibility):同时享有 Medicare 与 Medi-Cal,帮助低收入长者获得更多医疗福利 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】小型企業健康保險方案(SHOP)與專屬稅額抵免:透過 Covered California for Small Business,協助雇主團隊取得專屬稅額抵免 | BIEU LAM INSURANCE SERVICE | 林國彪保險

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。

分享本頁

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。