點評

點評 微信

微信 微博

微博【保險】什么是红蓝卡(Medicare)的核心四大组成部分? | BIEU LAM INSURANCE SERVICE | 林國彪保險

根据联邦法规,红蓝卡(Medicare)的 A、B、C、D 部分各自承保什么?

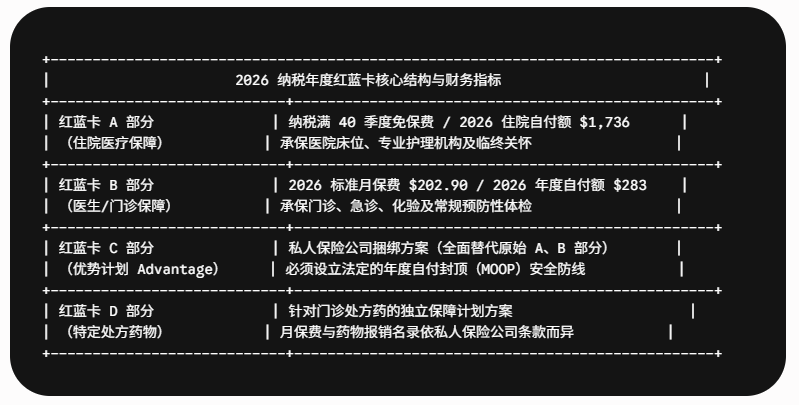

在联邦法定框架下,红蓝卡医疗保险被精细地划分为四个核心组成部分:A部分为住院保险,主要负责因病住院、专业护理机构关怀及临终关怀;B部分为医生医疗保险,承保医生门诊、门诊手术、预防性筛查以及耐用医疗设备;C部分即“联邦医疗保险优势计划”,是由私人保险公司运营的捆绑式合规保单;D部分则为独立处方药保险。其中,A部分与B部分被美国联邦医疗保险和联邦医疗救助服务中心(CMS)统称为“原始红蓝卡”(Original Medicare)。

理解这些不同部分的搭配逻辑,是防范未来理赔缺口及终身罚款的关键。迈入 2026 纳税年度,CMS 针对各项红蓝卡设定的最新保费与自付额标准要求企业主和家庭予以高度重视:

- 红蓝卡 A 部分(住院保险): 绝大多数在美国或其配偶累计工作纳税满 40 个季度的加州年长者,均可免保费享有A部分。但若需住院,2026年每个福利期(Benefit Period)的初始自付额为 $1,736。

- 红蓝卡 B 部分(医生医疗保险): 2026年的标准月保费调整为 $202.90,年度自付额为 $283。对于阿卡迪亚地区的很多高收入家庭或企业主,若其两年前的报税收入(MAGI)超过法定门槛,则需额外缴纳高收入附加费(IRMAA)。

- 红蓝卡 C 部分(优势计划 Advantage): 这是经 CMS 严格审批、由私人保险公司销售的替代型计划。它不仅承保 A 部分与 B 部分的所有项目,还强制设立了“年度最高个人自付限额(MOOP)”,并通常额外赠送牙科、眼科、听力及健身等原始红蓝卡不包含的福利。

- 红蓝卡 D 部分(处方药保险): 属于自愿购买的商业处方药保单,每家保险公司的受保药物目录(Formulary)和自付比例均有不同。

我应该如何选择适合我的红蓝卡方案?可以把它们组合起来吗?

红蓝卡的最佳配置完全取决于您个人的健康状况、财富结构以及对医生网络的需求。投保人通常面临两大战略抉择:一是保留“原始红蓝卡(A+B)”,并额外配置独立的“D部分处方药保单”以及私人商业“红蓝卡补充险(Medigap)”以冲抵自付额;二是直接放弃原始红蓝卡结构,整体转入全包式的“C部分优势计划(Medicare Advantage)”。

新晋年长者应该在什么时候、如何锁定制定的红蓝卡?

加州年长者满 65 岁时的“初始投保期”(IEP)是如何计算的?

初始投保期(Initial Enrollment Period,简称 IEP)是一个长达 7 个月的法定严格窗口期,这是年长者首次申请红蓝卡且免受逾期罚款的黄金时段。该窗口期以受益人 65 岁生日的那一个月为中心,向前涵盖 3 个月,向后顺延 3 个月。在这一区间内完成投保,能确保医疗福利无缝生效。

若由于信息脱节错过了 IEP 窗口,年长者将面临极其被动的终身罚款风险。例如,B部分逾期罚款规定,每延迟 12 个月投保,未来的月保费将永久性加收 10%;D部分处方药同样存在每月 1% 的累积终身罚款。对于圣盖博谷本地的华人企业主或多代同堂的家庭而言,何时从现有的公司团体医疗险(Group Health Plan)合规剥离、如何评定现有保险是否属于国税局认可的“可信赖承保”(Creditable Coverage),都需要极其精密的架构测算。林标保险的资深专家团队通过前瞻性的个人风险管理,为您提供严谨的时效把控,协助您避开所有隐形课税与罚金圈套,让您的退休岁月在稳健中扬帆远航。

有需要任何建議諮詢,請聯繫林國彪保險Bieu Lam Insurance 。我們另外有福地墓園,殯儀服務一站式協助。

免責聲明:本文內容僅供教育與資訊參考之用。保險政策條款、承保範圍及符合資格之要求可能會有所變動。具體的健康保險承保內容及保費補助資格,須以保險公司核保結果、收入審查及實際保險合同條款為準。

What Are the Four Core Parts of Medicare?

What do Medicare Parts A, B, C, and D cover under federal guidelines?

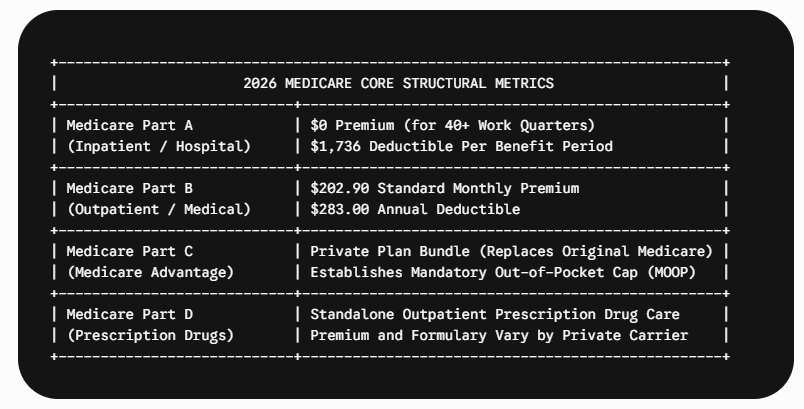

Under federal statutory frameworks, Medicare is divided into four distinct components: Part A covers inpatient hospital stays, skilled nursing, and hospice care; Part B covers outpatient medical services, doctor visits, and durable medical equipment; Part C represents private Medicare Advantage plans that bundle Parts A, B, and usually D; and Part D provides standalone prescription drug coverage. Together, Parts A and B are categorized by the Centers for Medicare & Medicaid Services (CMS) as Original Medicare.

Navigating these distinct categories requires careful planning to prevent coverage gaps or lifelong late-enrollment penalties. The premium and deductible limits for the 2026 calendar year require strict financial attention:

- Medicare Part A (Hospital Insurance): For most California seniors who have completed 40 quarters of qualifying U.S. work history, Part A is premium-free. However, it carries an inpatient hospital deductible of $1,736 per benefit period.

- Medicare Part B (Medical Insurance): Part B requires a standard monthly premium of $202.90 and carries an annual deductible of $283. High-income earners in hubs like Arcadia may face additional surcharges via the Income-Related Monthly Adjustment Amount (IRMAA) based on tax returns from two years prior.

- Medicare Part C (Medicare Advantage): These plans are managed by private, CMS-approved carriers. They replace Original Medicare structures, establish a vital Maximum Out-of-Pocket (MOOP) safety limit, and frequently integrate dental, vision, and wellness benefits.

- Medicare Part D (Prescription Drug Coverage): This optional program is run by private insurance companies to lower the cost of outpatient prescription medications, featuring distinct formularies and cost-sharing tiers.

Which Medicare part is right for me, and can I combine them?

The right Medicare structure depends on your personal health risks, budget constraints, and preferred doctor networks. Beneficiaries must choose between keeping Original Medicare (Parts A and B)—frequently pairing it with a standalone Part D plan and a private Medicare Supplement (Medigap) policy—or replacing that setup entirely with a comprehensive Medicare Advantage Plan (Part C).

When and How Should New Seniors Enroll in Medicare?

What is the Initial Enrollment Period (IEP) for California seniors turning 65?

The Initial Enrollment Period (IEP) is a strict seven-month window that serves as a senior's primary opportunity to register for Medicare without penalty. This statutory period begins exactly three months before the month you turn 65, includes your birth month, and extends for three months immediately following. Enrolling during this timeframe ensures your coverage starts promptly and prevents lifelong premium penalties.

Failing to register during the IEP can lead to significant financial consequences. For instance, the Part B late-enrollment penalty adds an extra 10% to your monthly premium for each full 12-month period you were eligible but remained uninsured. Similarly, Part D imposes a lifetime penalty of 1% per month for delayed sign-ups without creditable coverage. For local business owners and multi-generational families in the San Gabriel Valley, coordinating this transition requires analyzing active employer group health plans against federal guidelines. Our proactive personal risk management team monitors these enrollment timelines to prevent compliance errors, ensuring a smooth and secure transition into your retirement years.

版权归原作者所有。如有侵权请联系我们,我们将及时处理。

我精通國、粵、潮、越、英語,希望用您最舒適的語言與您溝通。我將協助個人、家庭及團體,提供健康保障、人壽保險、財務規劃,歡迎諮詢!竭誠為您服務。

- 【保險】加州小企业健康保险指南:企业主与管理者必读 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】解读“Enhanced Silver 87”计划:2025-2026年如何获得零保费、零自付额医疗保险 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】2026年加州个人医保强制规定:避免州税罚款的最终检查清单 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】双重资格(Dual Eligibility):同时享有 Medicare 与 Medi-Cal,帮助低收入长者获得更多医疗福利 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】小型企業健康保險方案(SHOP)與專屬稅額抵免:透過 Covered California for Small Business,協助雇主團隊取得專屬稅額抵免 | BIEU LAM INSURANCE SERVICE | 林國彪保險

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。

分享本頁

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。