點評

點評 微信

微信 微博

微博【保險】什么是中小型企业医疗保险税务抵免? | BIEU LAM INSURANCE SERVICE | 林國彪保險

在当今充满竞争的加州商业环境中,中小型企业主不仅面临着保留核心人才的压力,还必须应对日益增高的运营成本。作为立足阿卡迪亚(Arcadia)、服务全加州华人群体的全方位“一站全到位保险与理财服务”机构,林标保险(Bieu Lam Insurance)深谙本地企业主的痛点。我们致力将复杂的合规与税务政策转化为清晰、可信赖的战略指导,协助您在为团队配置全面商业医疗保险的同时,精准解锁联邦及加州法律赋予的专属税务抵免。这不仅是您对员工健康做出的长远投资,更是“保护您辛勤积攒的资产与家庭传承”的核心财富管理策略。

什么是中小型企业医疗保险税务抵免?

根据美国国税局(IRS)第 45R 条款,中小型企业医疗抵免如何运作?

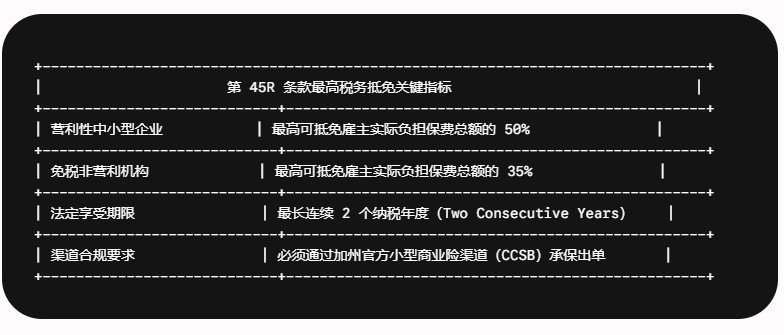

根据联邦税法第 45R 条款(Section 45R),符合条件的小型企业主若为员工提供合规的团体医疗保险,最高可获得相当于雇主所付保费 50% 的联邦税务抵免(Tax Credit);非营利免税组织最高可获得 35% 的抵免。该抵免不同于普通的税务扣除(Deduction),它能直接等额扣减企业应缴纳的联邦企业所得税,从而显著降低企业的运营净开支。

为了顺利通过承保及税务审核,加州企业必须满足严格的人员与薪资限制。该政策采用阶梯式(Sliding Scale)减免机制,越是初创、微型的企业,获得的抵免比例越高。核心评估指标包括:

- 全职等效员工数(FTE): 企业的全职等效员工总数必须少于 25人。

- 平均年薪限制: 2026 纳税年度的员工平均年薪须低于 $68,200(此标准随通胀逐年调整)。若想全额锁定 50% 的最高抵免额度,员工平均年薪须维持在 $34,100 或以下。

- 保费资助比例: 雇主必须建立合规的供款机制,且为每位参与保险的员工支付至少 50% 的单身保费(Single Premium)。

- 指定投保渠道: 企业所采购的团体健康險计划必须通过加州官方小型商业健康选项项目(Covered California for Small Business, 简称 CCSB)进行出单与绑定。

雇主可以连续多少年申请 Section 45R 税务抵免?

符合资格的小型企业雇主,在首次通过加州官方小型商业健康险市场(CCSB)为其团队投保后,最多只能连续 2 个纳税年度申请第 45R 条款的保费税务抵免。由于这一两年的法定窗口期不可逆转且无法暂停,企业主必须联合资深保险顾问进行精确的财务时机规划。

如何正确计算全职等效员工(FTE)以确保抵免资格?

用于小型企业健康险税务抵免的 FTE 官方计算公式是什么?

全职等效员工(FTE)的法定计算方法是:将所有全职和兼职员工全年的总工作时数相加(每名员工的计算上限为 2,080 小时),然后将该总时数除以 2,080。所得出的商数向下取整至最接近的整数,即为该企业在税务合规上的官方 FTE 数量。需要注意的是,企业主、合伙人及其直系亲属在法律上属于免除对象,不得计入其中。

在阿卡迪亚和圣盖博谷(San Gabriel Valley)的华人商业圈中,许多劳动力密集型企业(如餐饮、零售、物流仓储及进出口贸易)往往雇用大量兼职(Part-time)人员。由于未能正确理解 FTE 的换算机制,许多企业主误以为员工总人数超过 25 人便直接丧失了申请资格。相反,通过林标保险的结构化风险评估,我们可以帮助您剔除企业主家庭成员,并将兼职总工时科学换算。例如,一个拥有 30 名兼职员工的公司,经过精准折算后的 FTE 可能仅为 18 人,从而完全符合国税局的减免标准。我们为您量身定制贴合生命周期里程碑的综合保障方案,在严密防范加州劳工部(DIR)与国税局合规风险的同时,最大化您的企业现金流优势。

What is the Small Business Health Care Tax Credit?

How do small business health insurance tax credits work under Internal Revenue Code Section 45R?

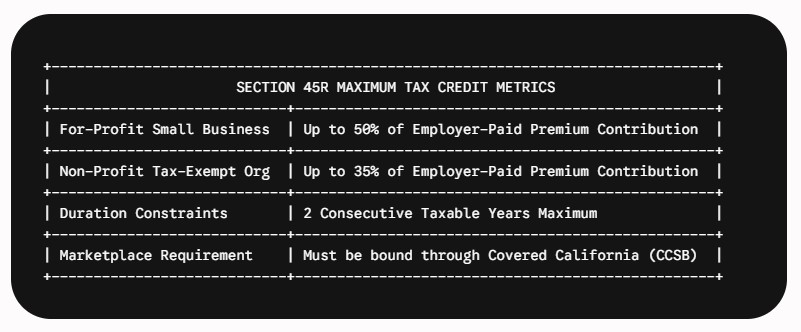

The Small Business Health Care Tax Credit under IRC Section 45R allows eligible small employers to claim a federal tax credit of up to 50% of their contributions toward employee health insurance premiums. For tax-exempt non-profit organizations, the maximum credit is capped at 35%. This credit acts as a direct dollar-for-dollar reduction of your corporate income tax liability, rather than a mere deduction, making group health plans substantially more affordable.

To qualify for this critical incentive, California businesses must satisfy strict demographic and financial criteria established by the Internal Revenue Service (IRS). The credit is structured on a sliding scale to maximize relief for micro-enterprises. The underwriting and regulatory parameters include:

- FTE Threshold: The enterprise must employ fewer than 25 Full-Time Equivalent (FTE) employees.

- Wage Limitations: For the 2026 tax year, the average annual wage across the workforce must be under $68,200 (adjusted for inflation). To secure the maximum 50% credit, average wages must remain at or below $34,100.

- Employer Contribution: The employer must establish a qualifying arrangement and contribute a minimum of 50% of the single premium cost for each enrolled team member.

- Marketplace Mandate: The coverage must be programmatically secured through a qualified state marketplace, such as Covered California for Small Business (CCSB).

How many years can an employer claim the Section 45R tax credit?

An eligible small business employer can claim the Section 45R health care tax credit for a maximum of two consecutive taxable years, beginning from the first year the employer utilizes the qualified small business marketplace exchange. Once this two-year statutory window closes, the credit expires, making strategic timing essential to optimize fiscal benefits.

How do you calculate Full-Time Equivalent (FTE) employees for the tax credit?

What is the formula for calculating FTEs for the small business tax credit?

The formula to calculate Full-Time Equivalent (FTE) employees involves totaling the annual hours worked by all part-time and full-time employees (up to a maximum of 2,080 hours per individual) and dividing that aggregate number by 2,080. The resulting quotient, rounded down to the nearest whole number, represents your official FTE count for tax compliance. Business owners, their spouses, and immediate family members are statutory exclusions and are not counted in this calculation.

Miscalculating the FTE metrics is a frequent compliance oversight that can trigger an unexpected disqualification or a reduction of the credit during a tax audit. For instance, an Arcadia-based retail firm or a logistics company in the San Gabriel Valley may employ 30 part-time workers, yet their aggregate hours might equate to only 18 FTEs, successfully preserving their tax eligibility. Conversely, because business owners, partners, and immediate family members are excluded from the numerator and denominator, specialized entity modeling is required. Bieu Lam Insurance provides comprehensive coverage tailored to your life's milestones and business growth, ensuring your group structures perfectly align with California Department of Insurance (CDI) and IRS guidelines.

版权归原作者所有。如有侵权请联系我们,我们将及时处理。

我精通國、粵、潮、越、英語,希望用您最舒適的語言與您溝通。我將協助個人、家庭及團體,提供健康保障、人壽保險、財務規劃,歡迎諮詢!竭誠為您服務。

- 【保險】加州小企业健康保险指南:企业主与管理者必读 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】解读“Enhanced Silver 87”计划:2025-2026年如何获得零保费、零自付额医疗保险 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】2026年加州个人医保强制规定:避免州税罚款的最终检查清单 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】双重资格(Dual Eligibility):同时享有 Medicare 与 Medi-Cal,帮助低收入长者获得更多医疗福利 | BIEU LAM INSURANCE SERVICE | 林國彪保險

- 【保險】小型企業健康保險方案(SHOP)與專屬稅額抵免:透過 Covered California for Small Business,協助雇主團隊取得專屬稅額抵免 | BIEU LAM INSURANCE SERVICE | 林國彪保險

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。

分享本頁

打開微信,使用 “掃描QR Code” 即可將網頁分享到我的朋友圈。